Proof of Address: The Small Requirement with Large Consequences

Proof of address appears routine. Yet behind this requirement lies a foundational assumption: that location infrastructure is stable and accessible.

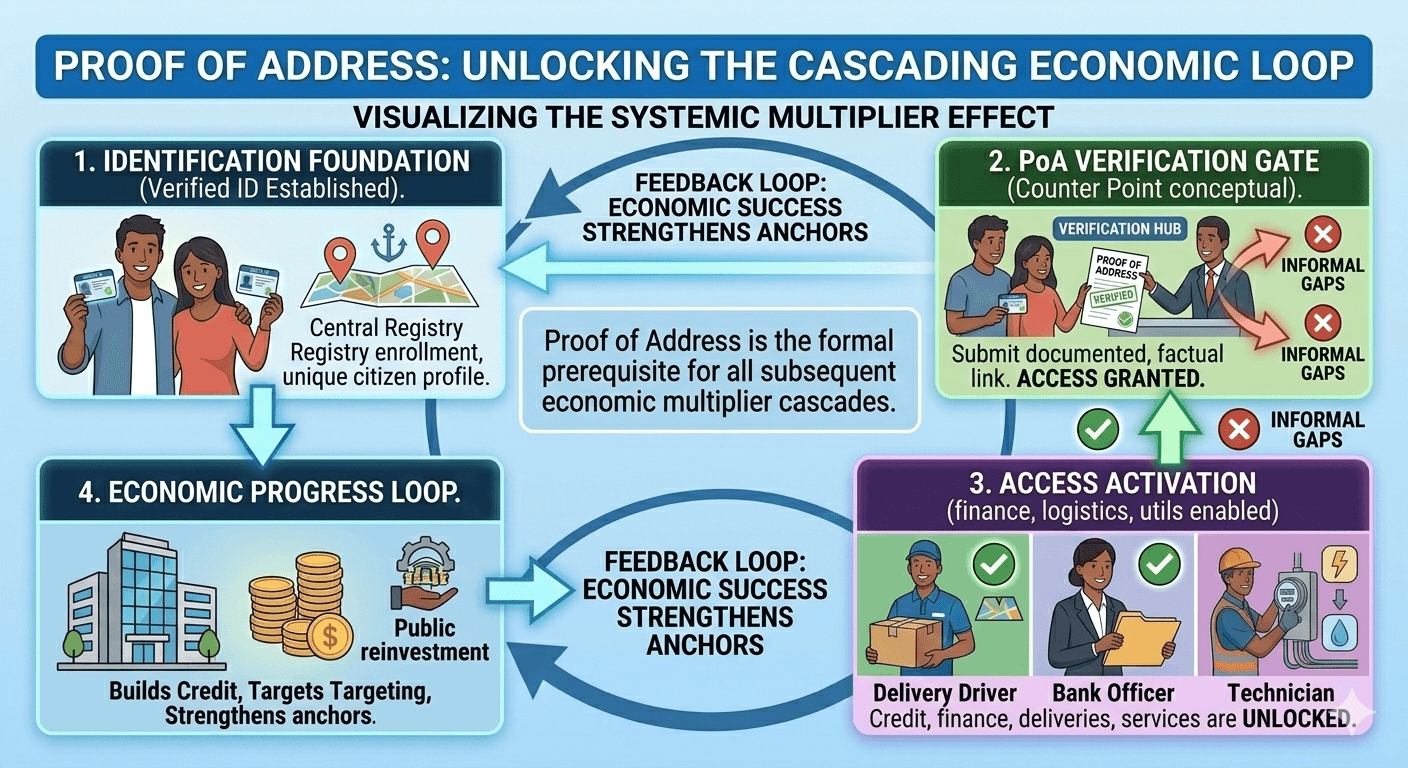

Introduction: A Routine Requirement

“Proof of address” appears in:

Bank onboarding forms

Telecom registration processes

Loan applications

School admissions

Government benefit programs

It is often treated as a minor administrative step.

In reality, it is a gatekeeper.

Why Institutions Require It

Financial institutions apply Know Your Customer (KYC) regulations to:

- Prevent fraud

- Reduce money laundering

- Verify residential stability

Location serves as a secondary anchor to identity.

Regulatory frameworks influenced by bodies like the Financial Action Task Force encourage robust customer verification processes.

Address becomes part of compliance infrastructure.

The Exclusion Effect

For individuals in:

- Informal settlements

- Subdivided rental units

- Recently migrated households

Obtaining acceptable proof of address can be difficult.

The World Bank’s Global Findex surveys consistently show documentation barriers as a reason for remaining unbanked.

A small administrative requirement can become a structural exclusion mechanism.

Informal Workarounds

When formal proof is unavailable, people may:

- Use a relative’s address

- Rely on informal attestations

- Use landmarks

- Avoid formal financial systems altogether

These workarounds weaken data integrity and increase systemic risk.

Business Registration and Entrepreneurship

Entrepreneurs often need:

- Registered business addresses

- Utility bills

- Lease agreements

If address systems lack precision or legal clarity, business formalization slows.

Address precision influences ease of doing business.

Conclusion: Administrative Detail, Economic Impact

Proof of address appears routine.

Yet behind this requirement lies a foundational assumption: that location infrastructure is stable and accessible.

When that assumption fails, economic participation narrows.